Understanding the Paperwork: The Claim Summary

After the adjuster’s visit, you’ll receive a claim summary. This is an important document that outlines the scope of work the insurance company has approved, the cost they’ve estimated, and the amount they will pay out. Take your time to review this document.

The claim summary will typically have a few key sections:

![]() ACV (Actual Cash Value) Payment: This is the initial check you’ll receive. It’s the depreciated value of your roof, meaning it accounts for the roof’s age and wear.

ACV (Actual Cash Value) Payment: This is the initial check you’ll receive. It’s the depreciated value of your roof, meaning it accounts for the roof’s age and wear.

Deductible: This is the amount you are responsible for paying out-of-pocket before your insurance coverage kicks in.

Deductible: This is the amount you are responsible for paying out-of-pocket before your insurance coverage kicks in.

![]() RCV (Replacement Cost Value): This is the total cost of the roof replacement, including all approved line items. You’ll receive the remaining balance of this amount, minus the ACV already paid, once the work is completed.

RCV (Replacement Cost Value): This is the total cost of the roof replacement, including all approved line items. You’ll receive the remaining balance of this amount, minus the ACV already paid, once the work is completed.

This process can feel a little complicated, but don’t worry. A reputable Top reviewed roofing company will help you understand every line item on that claim summary and ensure that all necessary repairs are included.

The Incredible Journey of Home Insurance

We know that the whole process—especially the insurance part—can feel a little bit like a mystery. So, let’s peel back the curtain and take a look at the fascinating history of how we got to where we are today.

Understanding where home insurance came from isn’t just a fun history lesson; it gives you a deeper appreciation for the protection it provides and why certain aspects of your policy exist. It’s a story of communities coming together, of learning from devastating events, and of a whole industry evolving to meet our needs.

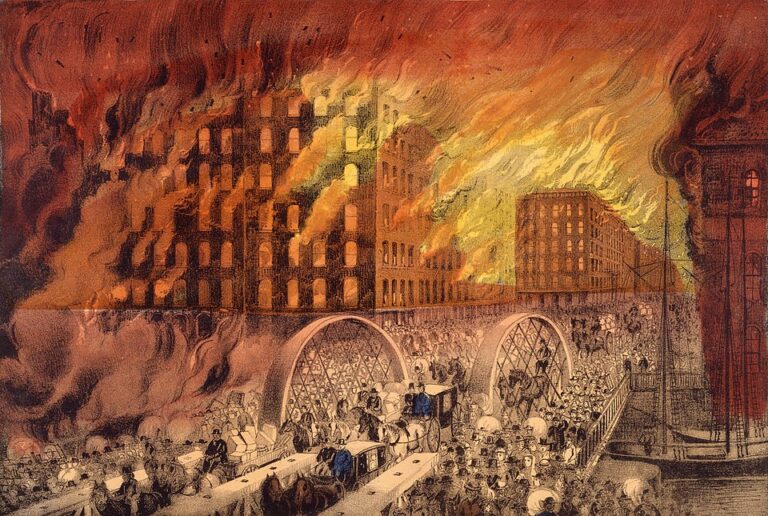

From Volunteer Brigades to Benjamin Franklin

The earliest ideas of insurance in America were born out of necessity, long before we had formalized companies and policies. Think about our colonial towns: most buildings were made of wood, packed closely together, and lit by candles. Fire was a constant, terrifying threat. When a fire broke out, the entire community would rush to help, passing buckets of water and tearing down neighboring buildings to create a fire break. This was the original “mutual aid” system—an unwritten understanding that your neighbors would help you, and you would help them.

The earliest ideas of insurance in America were born out of necessity, long before we had formalized companies and policies. Think about our colonial towns: most buildings were made of wood, packed closely together, and lit by candles. Fire was a constant, terrifying threat. When a fire broke out, the entire community would rush to help, passing buckets of water and tearing down neighboring buildings to create a fire break. This was the original “mutual aid” system—an unwritten understanding that your neighbors would help you, and you would help them.

This informal system started to get more organized. In 1736, Benjamin Franklin, ever the innovator, founded the Union Fire Company in Philadelphia, one of the first volunteer fire departments in America. These companies were a huge step forward, but they didn’t offer financial protection. The threat of a fire still meant total financial ruin.

This informal system started to get more organized. In 1736, Benjamin Franklin, ever the innovator, founded the Union Fire Company in Philadelphia, one of the first volunteer fire departments in America. These companies were a huge step forward, but they didn’t offer financial protection. The threat of a fire still meant total financial ruin.

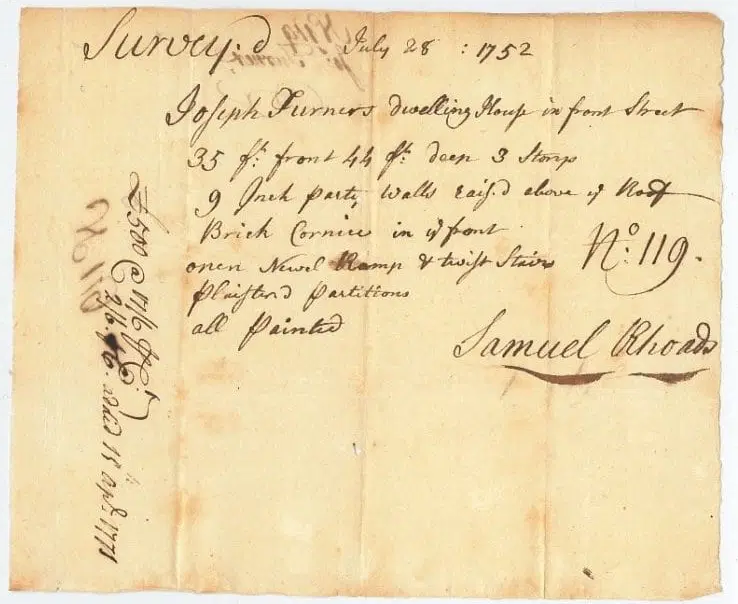

Recognizing this gap, Franklin went on to help found the Philadelphia Contributionship in 1752. This was a truly groundbreaking moment. It was the first mutual fire insurance company in the colonies. The idea was simple but powerful: members paid into a common fund, and if any member’s house burned down, the fund would be used to help them rebuild. They even refused to insure buildings deemed too risky, like those with certain types of wooden chimneys, setting the stage for modern risk assessment and underwriting.